Not All SaaS Are Created Equal

Axon’s Q4 2025 Earnings Just Proved It

Last week, Axon reported Q4 2025 earnings.

Revenue: $797 million. Up 39% year over year.

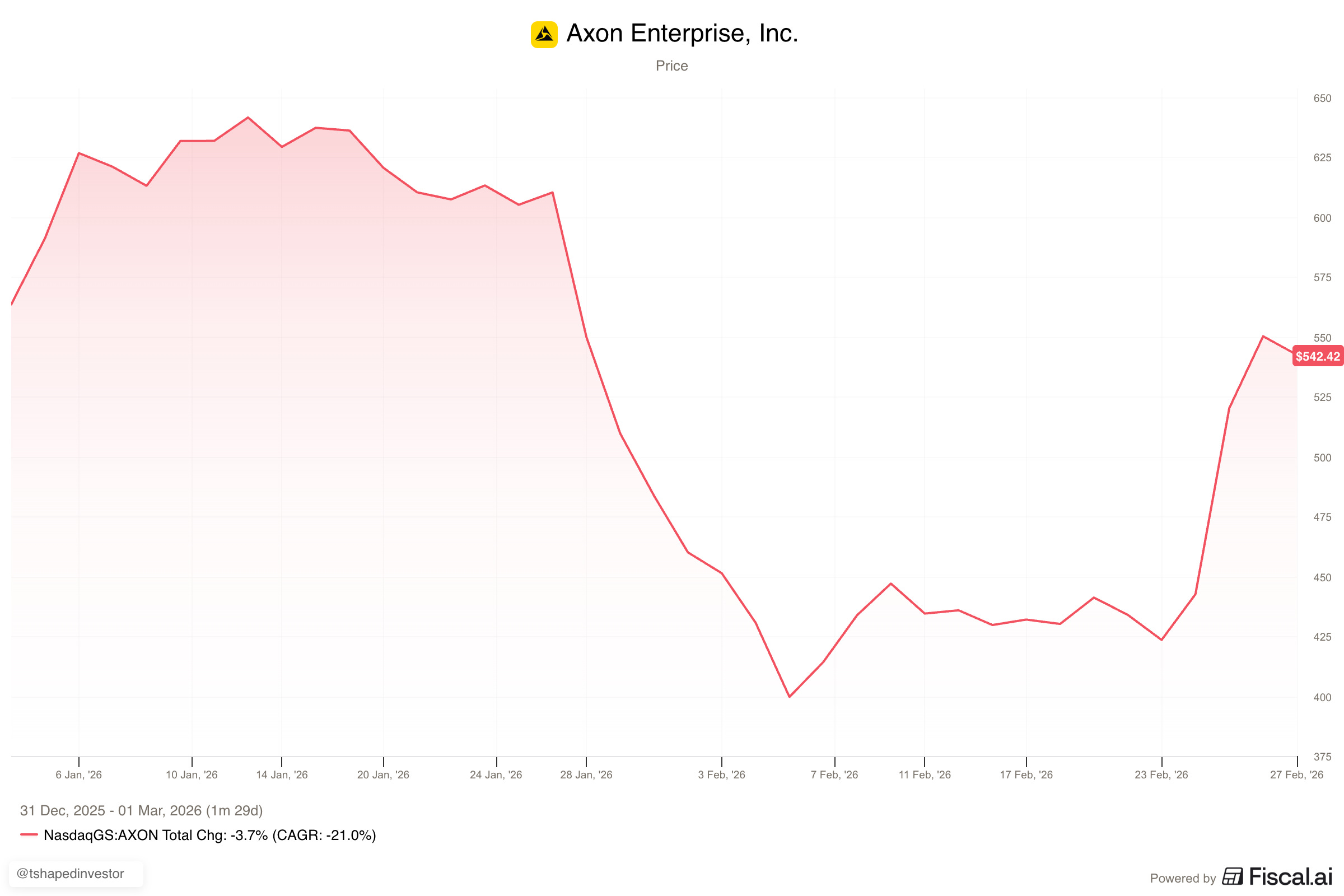

The stock had been in freefall for weeks before that. From a high of ~$635 in early January, it crashed to ~$405 by early February — a 36% drawdown in under a month. Wall Street had turned deeply nervous: worried that AI would commoditize their software, worried that the hardware-attached business model was a liability, worried that the valuation couldn’t be justified.

Then the earnings dropped. The stock ripped from ~$450 to ~$520 in a single session.

Every one of those fears turned out to be wrong.

But here’s what I actually want to talk about today: not the headline numbers, but why Axon’s SaaS business is one of the most misunderstood, and now one of the most validated, software businesses in the public markets.

Because not all SaaS are created equal.

(If you haven’t checked it out yet, head over to moatalytics.ai and sign up for early access. It’s coming soon, and yes, Multibagger Insights subscribers get first dibs.)

The Fear That Wasn’t

Let me set the scene.

Over the past 12 months, there was a genuine narrative forming that AI would eat Axon’s lunch. The logic went something like this: if AI can write police reports automatically, why would agencies pay a premium for Axon’s software? Wouldn’t some scrappy startup undercut them with a cheaper model?

This is the same misunderstanding I wrote about last week with ServiceNow — the confusion between the model and the moat.

Axon doesn’t just sell software. They sell software that is deeply embedded into the evidence management workflows, the body camera ecosystems, the TASER networks, and the real-time operations platforms of thousands of public safety agencies. Their AI doesn’t sit on top of some generic data. It sits on top of 60 million hours of body-worn camera footage, billions of data points about how public safety workflows actually operate, and a customer base that signed 5-10 year contracts.

That’s not a software business waiting to be disrupted by AI. That’s a software business that AI is actively making more valuable.

The market missed this. And for a while, the stock paid the price.

The SaaS Engine Hiding Inside a Hardware Company