Which Software Stock Survives the AI Transition?

ServiceNow vs. Salesforce vs. Adobe vs. GitLab: My Software Stock Pick for 2026

The fiscal year 2025 has been characterized by a historic decoupling within the technology sector, dominated by semiconductor manufacturers and hyperscalers. Data centers owners, operators, and suppliers have experienced an unprecedented capital expenditure super-cycle driven by Generative AI training demand. However, the application software layer faced a brutal compression in valuation multiples. This divergence was not merely a function of interest rate sensitivity but reflected a deeper existential anxiety among institutional investors: the fear that Artificial Intelligence constitutes a deflationary force for the traditional “per-seat” SaaS business model.

For two decades, the enterprise software investment thesis was predicated on headcount expansion. As companies grew, they hired more employees, necessitating more licenses (seats) for Salesforce, Adobe, and ServiceNow. The emergence of agentic AI in 2025 disrupted this linearity. If an AI agent can perform the workflow of three human employees, the terminal value of seat-based revenue streams becomes theoretically capped, if not negative. Consequently, 2025 became a year of “AI Indigestion,” where software equities stagnated as the market waited for evidence of monetization that could offset the potential cannibalization of human seats.

Has the market taken this bearish narrative too far?

We are witnessing the early stages of a successful transition to “Consumption-Based” and “Hybrid” business models that allow these traditional SaaS businesses to monetize the work rather than the worker. The sell-off has created significant dislocations between intrinsic value and market price, particularly in names where the “death by AI” narrative is most acute.

This report evaluates four software stocks—GitLab (GTLB), ServiceNow (NOW), Adobe (ADBE), and Salesforce (CRM)—to identify the superior risk-adjusted capital allocation for 2026. By synthesizing reverse Discounted Cash Flow (DCF) models, analyzing the subtext of bearish analyst interrogations, and scrutinizing the mechanics of their new AI pricing models, we arrive at a definitive conclusion.

The Macro-Thematic Headwind

Throughout 2025, Chief Information Officers (CIOs) froze application layer spending to fund experimental AI infrastructure projects. As noted by HSBC analysts, the market focused entirely on the “picks and shovels” (chips), leaving the software vendors that utilize those chips to languish. This pause was exacerbated by a lack of immediate ROI from early AI deployments. As companies moved from “hype” to “implementation,” they encountered the “Last Mile” problem—getting AI to work reliably in complex enterprise environments is difficult. This led to what Salesforce management described as a “coiled spring” dynamic: the demand is present, but the purchasing trigger was delayed until late 2025, creating a backlog of deal activity that is only now beginning to release.

The “Seat” vs. “Consumption” Existential Crisis

The central intellectual conflict determining valuation in this sector is the transition of business models. The market perceives the “Per User/Per Month” model as a liability. If AI efficiency leads to a 20% reduction in the global knowledge workforce, seat-based revenue contracts. To counter this, every company in this doc pivoted in 2025 toward consumption or hybrid models:

Salesforce introduced Agentforce, pricing it at $2 per conversation or via Flex Credits. This creates a direct correlation between revenue and the outcome of the software (a resolved ticket) rather than the tool (the login access).

Salesforce’s new Agentic Enterprise License Agreement (AELA) gives customers unlimited use of consumption‑based products such as Agentforce, Data 360/Data Cloud, and MuleSoft for a fixed fee over two or three years.

Salesforce's shift from $2 per conversation to Flex Credits and eventually AELA represents an evolution from rigid, event-based billing to a more granular, outcome-driven consumption model.

ServiceNow introduced Pro Plus, which utilizes a hybrid mechanism. It charges a premium on the seat license but meters the usage of “Now Assists” (AI interactions) via tokens. This protects the baseline revenue (the seat floor) while capturing the upside of heavy AI usage.

Adobe launched Generative Credits, a metering system for its Firefly models. Usage of these credits grew 3x sequentially in late 2025, proving that creative professionals are consuming compute at an accelerating rate.

GitLab is shifting to a Hybrid Seat + Usage model with its Duo Agent Platform. This is critical because AI coding assistants theoretically reduce the need for junior developers, the primary seat-holders in DevSecOps.

The bearishness in stock performance reflects the uncertainty of this transition. Consumption revenue is volatile and difficult to forecast. Investors hate uncertainty. However, I think that for the winners, this transition will expand the Total Addressable Market (TAM) by unlocking budget previously allocated to human labor wages, a pool significantly larger than IT software budgets.

ServiceNow (NOW)

Financial Performance

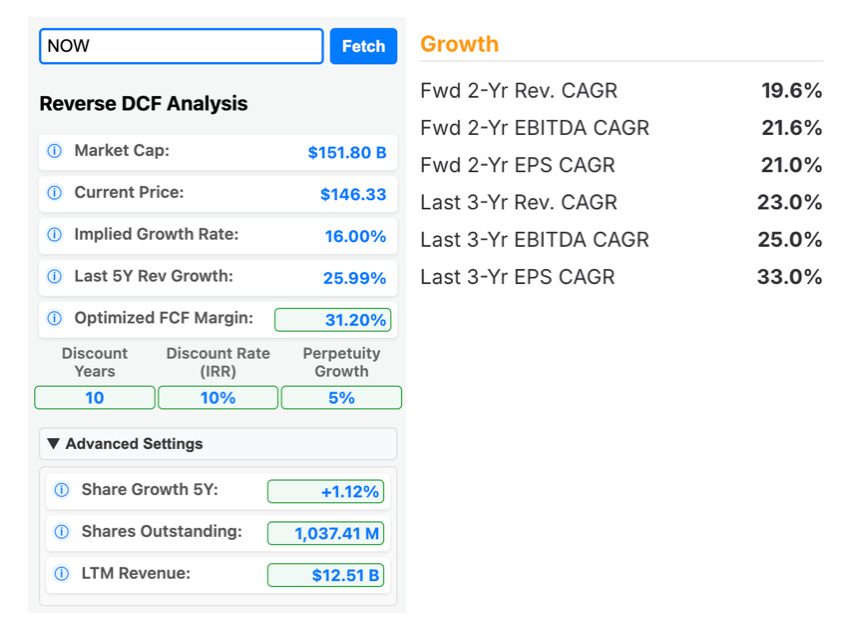

ServiceNow has distinguished itself as the “Execution Machine” of the sector. In a year where peers struggled to break into double-digit growth, ServiceNow reported Q3 2025 subscription revenues of $3.299 billion, representing 21.5% year-over-year growth (20.5% in constant currency). Total revenue reached $3.41 billion, beating analyst estimates by 1.4%.

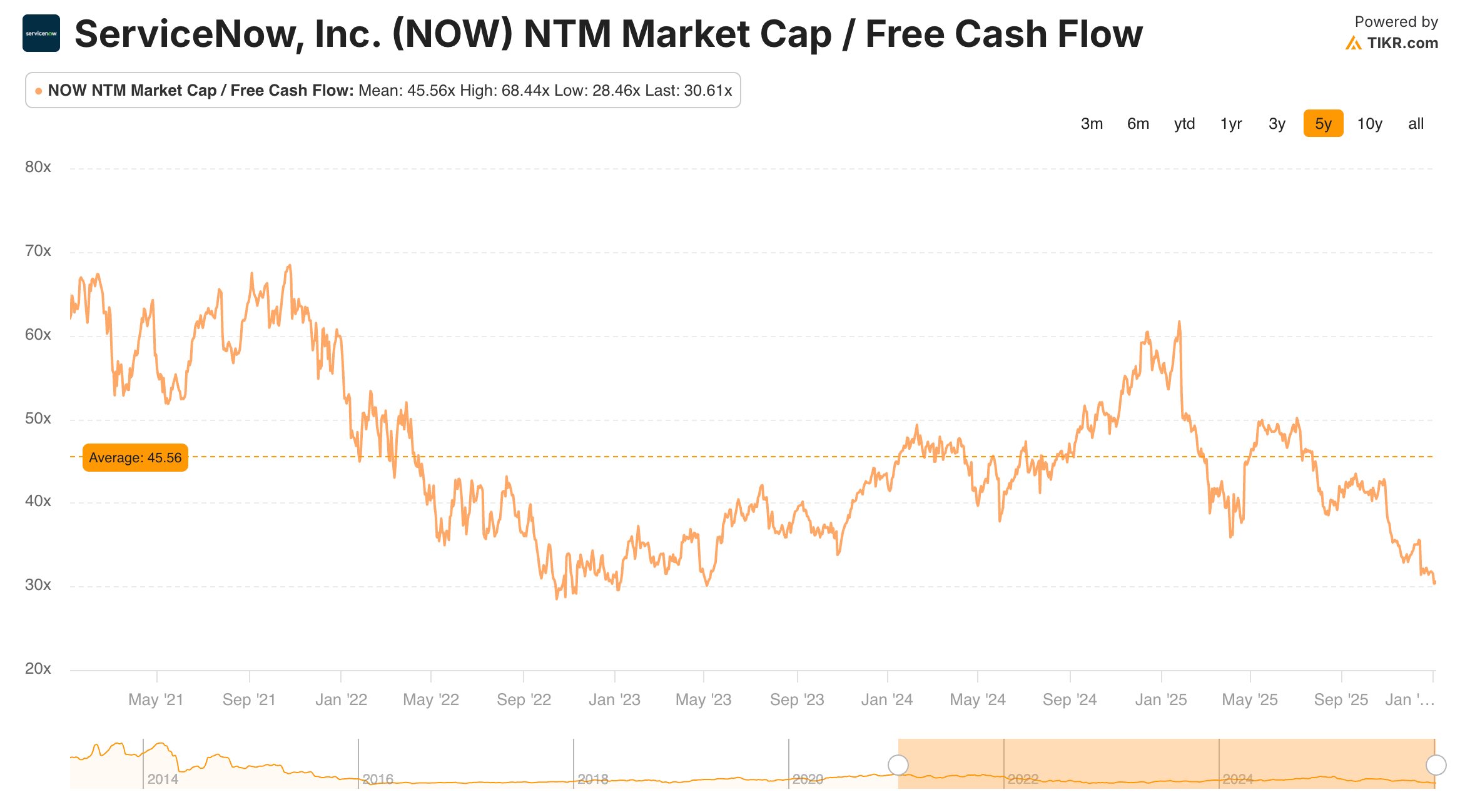

More impressively, the company achieved this while expanding profitability. Non-GAAP operating margins hit 31%, and the company raised its full-year guidance for both subscription revenue and free cash flow margin. The “Rule of 50” (Growth + Margin > 50) is alive and well at ServiceNow, a rarity for a company with a $154 billion market capitalization (Image 2). The company’s Current Remaining Performance Obligations (cRPO)—a proxy for near-term revenue—grew at 21%, signaling that the growth runway remains intact despite the law of large numbers.

AI Strategy: The “Pro Plus” Monetization Engine

ServiceNow’s AI strategy is the most coherent among the group. By launching the Pro Plus SKU, they effectively forced an upgrade cycle across their installed base. Management reported that the Pro Plus attach rate improved sequentially in Q3 2025, and 1,700 customers were live on “Now Assist”.

The genius of the Pro Plus model lies in its hybrid pricing. Unlike Salesforce, which risks cannibalizing seats with its consumption-only Agentforce agents, ServiceNow bundles the AI capability into the seat license at a 60% premium, with a consumption cap (tokens) that triggers overages. This ensures that even if a customer reduces headcount slightly, the Average Revenue Per User (ARPU) uplift from the remaining seats more than compensates. Analysts noted a 55x increase in AI consumption, validating that the product is delivering value and not just shelfware.

Bearish Analyst Scrutiny

Despite the stellar results, the Q3 2025 earnings call revealed specific anxieties from the sell-side community, which kept a lid on the stock price since then.

The Federal Spending Concern: Analyst Samad Samana questioned the level of “prudence” baked into the guidance regarding the U.S. federal government shutdown.13 The federal vertical is a massive growth driver for ServiceNow (up 30% in Q3), and any disruption there disproportionately affects the cRPO numbers. Management admitted to being conservative, which investors interpreted as a potential signal of slowing deal velocity.

The Renewal Cohort Cliff: Analyst Alex Zukin focused on the large Q4 renewal cohort, asking if it presented a “headwind” to growth rates. The concern here is structural: during the pandemic (2020-2021), ServiceNow signed massive 3-year deals. As these come up for renewal in late 2024/2025, there is a fear that customers, now focused on efficiency, might downsize their commitments. Management’s response—that they pulled forward deals into Q3—was reassuring but highlighted the lumpiness of enterprise sales cycles.

The Hype vs. Reality Gap: Zukin also pressed on “consumption vs. utilization,” seeking confirmation that the AI credits were actually being burned and not just sitting in accounts. This is the central skepticism of 2025: are we in an AI bubble? CEO Bill McDermott’s anecdote about a client killing 900 Proof-of-Concepts (PoCs) to consolidate on ServiceNow suggests the company is benefiting from “tool sprawl” consolidation, a deflationary force for competitors but an inflationary one for the platform winner.

Valuation Analysis

The Reverse DCF analysis for ServiceNow indicates a market that is pricing the asset with high precision, leaving little room for error but offering fair value for quality. At a price of ~$146, the implied growth rate is ~16% for a 10% IRR with and 5% perpetuity growth.

Despite a massive Market Cap of ~$150 billion, ServiceNow maintains a Forward 2-Year Revenue CAGR of 19.6%. Maintaining ~20% growth at this scale is statistically improbable and speaks to the immensity of its Total Addressable Market (TAM). Given this optimistic growth vs implied growth of 16%, ServiceNow valued attractively.

Last Twelve Months (LTM) Gross Margin of 78.1% and an LTM EBITDA Margin of roughly 33.5%. The Forward 2-Year EBITDA CAGR is 21.3%, indicating that profit growth is outpacing revenue growth—a classic signal of margin expansion and operational discipline.

ServiceNow trades at almost at lowest 5Y FCF multiple.

Salesforce (CRM)

Financial Performance

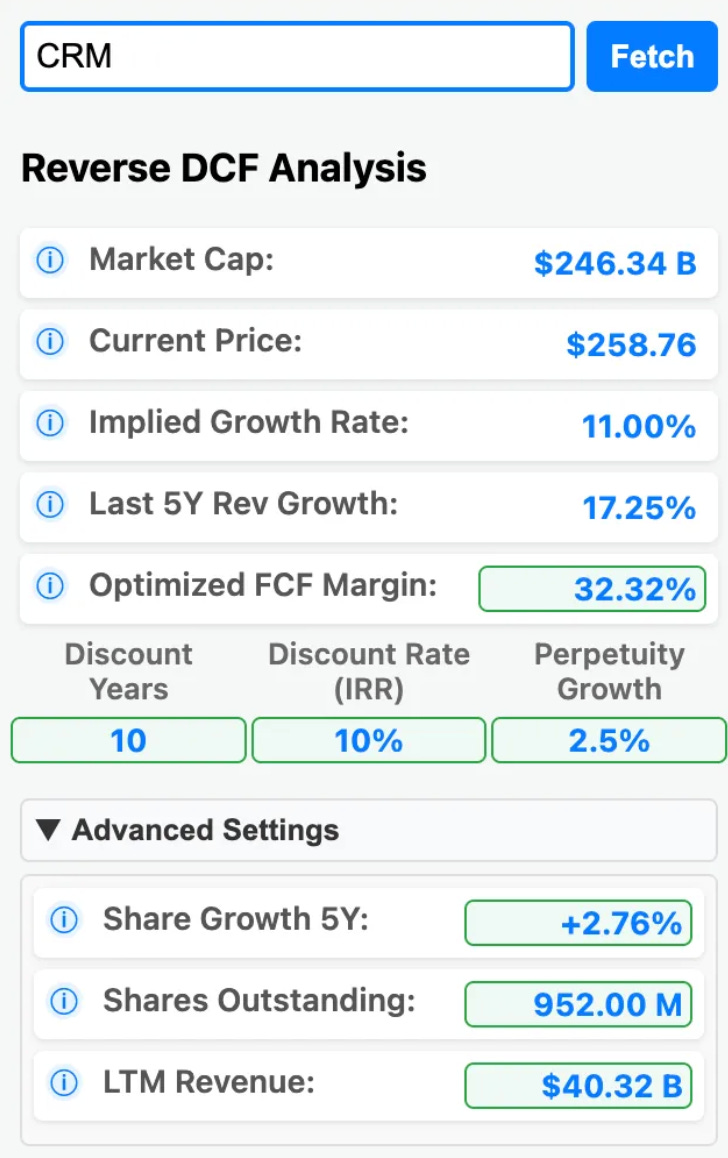

Salesforce’s fiscal 2026 (calendar 2025) narrative is one of maturation and efficiency, but arguably stagnation on the top line. In Q3, the company reported revenue of $10.28 billion, an 8.7% year-over-year increase. While this beat low expectations, single-digit growth for a “growth” stock is a severe de-rating event.

However, the margin story is undeniable. Non-GAAP operating margins expanded to 35.5%. Salesforce has effectively transformed into a cash-generating utility. The Data 360 platform ingested 32 trillion records (up 119% YoY), indicating that while revenue growth is slow, the platform’s “data gravity” is increasing.

AI Strategy: The Agentforce

Salesforce’s entire future rests on Agentforce. The company has gone all-in on the concept of autonomous agents. Salesforce mentioned Agentforce more than 35 in the Q3 FY26 earnings call transcript. The pricing model—$2 per conversation —is the most aggressive consumption pivot in the sector.

The risk here is profound. By charging per conversation, Salesforce invites a direct ROI calculation on every interaction. If an agent fails to resolve a ticket, the customer disputes the charge. Furthermore, this model cannibalizes the Service Cloud “per seat” model. If Agentforce works, customers need fewer human service agents. Salesforce is betting that the volume of automated conversations will dwarf the lost seat revenue.

The Agentic Enterprise License Agreement (AELA) is Salesforce’s strategic pricing model introduced in late 2025 to simplify the procurement of AI agents. It shifts away from complex "pay-per-conversation" or token-based billing toward a flat-rate, seat-based model that provides unlimited usage of Salesforce’s agentic AI capabilities for a predictable fee.

Bearish Analyst Scrutiny

The Q3 2026 earnings call was contentious, with analysts challenging the core tenets of Salesforce’s AI moat:

The “Build vs. Buy” Dilemma: Analyst Keith Weiss (Morgan Stanley) asked the most dangerous question: Why would a customer pay Salesforce for AI when they can build their own agents using open-source LLMs?. This questions the very existence of the application layer in an AI world. Management’s defense—that the context (customer data) resides in Salesforce—is valid, but the friction of the $2 price point makes “building your own” attractive for large enterprises.

Infrastructure Competitiveness: Analyst Brad Zelnick (Deutsche Bank) questioned Salesforce’s right to win in infrastructure against AWS and Azure. Salesforce manages over $10 billion in infrastructure-like revenue, but can they compete on compute costs with the hyperscalers?

Valuation Analysis

The Reverse DCF analysis for Salesforce indicates a market that is pricing the asset with moderate expectations, demanding execution but offering potential upside if efficiency targets are met. At a price of ~$259, the implied growth rate is 11.00% for a 10% IRR and 2.5% perpetuity growth.

With a Market Cap of ~$246 billion, Salesforce maintains a Forward 2-Year Revenue CAGR of 10.2%. While this top-line forecast slightly trails the implied growth of 11.00%, the story shifts when looking at profitability. The Forward 2-Year EPS CAGR is 13.4%, meaning the market’s implied expectations are well within the company’s projected earnings growth capabilities. Given this earnings strength vs implied growth of 11%, Salesforce is valued fairly on a profit basis.

Last Twelve Months (LTM) Gross Margin is 77.7% and LTM EBIT Margin is 22.0%. The Forward 2-Year EBITDA CAGR is 12.2% compared to Revenue CAGR of 10.2%, indicating that profit growth is outpacing revenue growth—a classic signal of margin expansion and operational discipline.

Adobe (ADBE)

Financial Performance

Adobe has been the punching bag of the “Generative AI” narrative. The stock fell ~30% over the last year on the thesis that Midjourney and OpenAI would democratize creativity and render Photoshop obsolete.

Yet, the financials contradict this death narrative. In Q4 2025, Adobe delivered record revenue of $6.19 billion, growing 10% year-over-year. Operating cash flows were a record $3.16 billion. The company aggressively repurchased 7.2 million shares, signaling that management sees the stock as deeply undervalued.

AI Strategy: The “Firefly”

Adobe’s defense is Firefly, its proprietary, commercially safe generative AI model. Unlike open models that scrape copyrighted data (creating legal liability for enterprise users), Firefly is trained on Adobe Stock images: this commercial safety is claimed to be a moat — I disagree.

Adobe introduced Generative Credits to monetize this usage. In Q4, credit consumption increased 3x quarter-over-quarter. This proves that instead of fleeing to Midjourney, professional creatives are using AI inside the Adobe workflow to accelerate their output. The “Generative Credit” model is a metered consumption layer on top of the Creative Cloud subscription, similar to ServiceNow’s model.

Bearish Analyst Scrutiny

The skepticism on the calls was palpable:

Usage vs. Revenue: Analyst Tyler Radke pointed out that while “generations” (images created) were high (4 billion), the number had stayed flat for two quarters. He essentially asked: “Is usage stalling, and where is the revenue?”. The fear is that AI features are just “table stakes” to keep customers from churning, rather than a driver of new net revenue.

The “Canva” Threat: Analyst Alex Zukin highlighted the competitive pressure in the “down market” (non-professionals), noting that competitors like Canva have 50 million Monthly Active Users (MAUs). The concern is that while Adobe wins the professionals, it loses the next generation of casual creators who find Photoshop too complex and expensive.

Coopetition with Meta: Analysts also worried about Meta’s AI ad tools overlapping with Adobe’s GenStudio. If Meta allows advertisers to generate creative assets directly in the Ad Manager, why do they need Adobe?

Valuation Analysis

The Reverse DCF analysis for Adobe indicates a market that is pricing the asset with extreme pessimism, essentially valuing the company as if it will barely grow despite its dominant market position. At a price of ~$336, the implied growth rate from reverse DCF assumes less than GDP growth needed for 10% IRR.

Despite a Market Cap of ~$141 billion, Adobe maintains a Forward 2-Year Revenue CAGR of 9.3%. This creates a massive disconnect: the market is pricing in 1% growth while analysts expect nearly 10%. Furthermore, the Forward 2-Year EPS CAGR is 12.2%, suggesting that share buybacks and margin management will drive double-digit earnings growth. Given this consensus growth vs implied growth less than GDP, Adobe is valued very attractively.

Last Twelve Months (LTM) Gross Margin is an impressive 89.3% and LTM EBIT Margin is 36.6%, highlighting its software monopoly economics. The company trades at a Next Twelve Months (NTM) EV/EBITDA of 11.28x and an NTM P/E of 14.32x, multiples that are historically low for a high-margin compounder of this quality.

GitLab (GTLB)

Financial Performance

GitLab remains the “Growth” play of the cohort. In Q3 2025, revenue grew 25% year-over-year to $244.4 million. However, it is the only company in this list that is not a GAAP profitability fortress, although it is generating non-GAAP operating income (18% margin).

AI Strategy: The “Duo” Hybrid Model

GitLab is at the epicenter of the “AI writes code” disruption. To capture value, they are shifting to a Hybrid Seat + Usage model. The Duo Agent Platform usage has increased 6x. This shift is mandatory; if AI makes developers 10x more productive, companies will hire fewer developers. GitLab must monetize the compute of the AI to offset the loss of seats.

Bearish Analyst Scrutiny

NRR Decay: Analyst questions focused on the drop in Net Revenue Retention (NRR) to 119% from 121%. In the SaaS world, NRR is the holy grail. A declining NRR suggests that the “expand” portion of “land and expand” is hitting friction, likely due to seat contraction.

Public Sector Weakness: Management cited “softness in the US public sector” as a headwind. For a DevSecOps company, government contracts are usually sticky and reliable; weakness here is a red flag for execution issues.

Valuation Analysis

The Reverse DCF analysis for GitLab indicates a market that is pricing the asset with significant caution, implying that its hypergrowth phase will decelerate rapidly. At a price of ~$35.57, the implied growth rate is 11.00% for a 10% IRR and 5% perpetuity growth.

With a Market Cap of ~$6 billion, GitLab maintains a Forward 2-Year Revenue CAGR of 22.0%. This reveals a stark disconnect: the market is pricing in ~11% growth while consensus estimates are double that figure at 22%. Furthermore, the Forward 2-Year EBITDA CAGR is a massive 54.6%, suggesting that as the company scales, its bottom-line profitability is expected to explode upwards. Given this growth profile vs implied growth of 11%, GitLab appears undervalued if it can hit these consensus targets.

Last Twelve Months (LTM) Gross Margin is an elite 88.0%, which provides the fuel for long-term free cash flow. While the LTM EBIT Margin is currently negative at (8.5%), the rapid EBITDA growth forecast confirms the company is at a critical inflection point, transitioning from pure growth to profitable growth.

GitLab trades at a Next Twelve Months (NTM) EV/EBITDA of 26.93x and an NTM P/E of 37.59x. While these multiples are optically higher than mature peers, they are rational for a company in the early innings of a “J-curve” profit inflection.

My Thoughts as An Engineer